Are we looking at a major market meltdown?

Stocks are succumbing to selling pressure of at type not seen since 2012. Yes, it's been that long.

After a meteoric rise in 2013, fueled by the apparent never-ending flow of cheap money from the Federal Reserve and the Bank of Japan, the Dow Jones industrial average is already down nearly 1,200 points from its high on New Year's Eve -- and by all indications, it's got further to fall. Selling on Monday accelerated late in the trading dow with the Dow falling more than 300 points by 3 p.m.

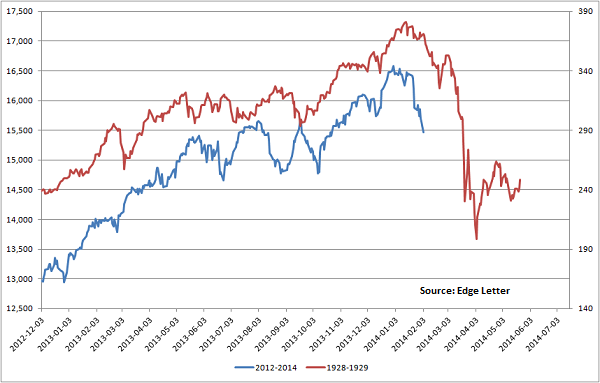

In fact, with the Dow marching in eerie lockstep with the run up to the 1929 market crash, as shown in the chart below, we could be looking at a complete wipeout of the 2013 market gains by March or April if the parallel pattern, known in charting as the price analog, holds.

Buckle your seat belts. Things are going to get exciting.

Price analogs, like much in the field of technical or chart analysis, are based on the fact that people, whether now or in the 1920s, are susceptible to the same emotional biases when they make buy or sell decisions. Old highs and old lows provide resistance and support because people are more sensitive to losses and breaking even than they are to gains, for instance.

As a result, a regression analysis shows that the current market behavior can be nearly 90 percent explained by what happened in 1929. That's an incredibly tight relationship, statistically speaking, for something that happened so long ago.

It's worth remembering that bond buying stimulus from the Fed in the late 1920s helped fuel excessive optimism and unsustainable market gains; so the analog isn't just based on price.

But the fundamentals are looking tough as well, with growth in U.S. factory activity slowing at a rate not seen since 2011. A cavalcade of concerns has replaced the quiet strength that seemed so resilient just a few weeks ago.

The Fed is pulling back on its bond buying programs, with the taper taking the "QE3" monthly bond buying pace down $20 billion to $65 billion as the unemployment rate drops faster than policymakers expected (largely, because people are leaving the workforce). And with inflation causing problems in Japan, as the trade deficit grows on higher food and fuel import prices as wages fail to keep up, the Bank of Japan looks less and less likely to expand its own bond buying program this spring.

As a result, the tide of cheap money is receding. And that's causing problems in the emerging markets as capital flees -- the subject of my recent article.

I see three potential accelerants heading into February that could keep the pressure on stocks.

First, the emerging market currency crisis is quickly spinning out of control. Last week's surprise interest rate hike by Turkey, taking rates from 7.75 percent to 12.5 percent in an effort stabilize their currency, failed to halt the slide. We also saw rate hikes by India and South Africa. The problem is that raising rates, which is the textbook cure for capital flight and inflation (the problem being faced in emerging market countries), results in stock market losses, a weaker economy, and higher credit defaults.

If the 1997 Asian crisis is any guide, we're going to see bailouts from the International Monetary Fund before this settles.

Second, the market is vulnerable to panic selling because bullish sentiment was so high. In fact, levels had reached bullish extremes not seen since the lead up to the 1987 market crash. Margin debt had swelled to record highs while available cash had dwindled to nil. The Nasdaq Composite hasn't closed below its 20-week moving average since 2012, enjoying an unblemished uptrend last year of a kind not seen since the final stage of the dot-com bubble. Additional price declines will be necessary to restore the balance between greed and fear.

Finally, additional budget battles loom in Washington. As soon as February 28, the U.S. Treasury will effectively run out of cash as it hits the drop-dead debt ceiling date. According to Treasury Secretary Jacob Lew, it would jeopardize Social Security payments and military pay unless action is taken. Democrats and Republicans have repeatedly clashed on the debt ceiling over the last few years.

Add it all up, and investors need to remain cautious and defensive. I continue to recommend a focus on cash or U.S. Treasury bonds (which, ironically, do well during debt ceiling fights). The leveraged Direxion 3x Treasury Bond Bull (TMF) is up more than 14 percent since I added it to my Edge Letter Sample Portfolio on January 10.

There are also opportunities on the short side for more aggressive traders such as Brazilian steelmaker Companhia Siderurgica Nacional (SID), which is down 14 percent since I added a short position on January 23.

Disclosure: Anthony has recommended TMF and SID short to his clients.

See www.gooddeedsmall.com

No comments:

Post a Comment